hello@infinity-globus.com

hello@infinity-globus.com +1(754)-258-4994

+1(754)-258-4994

Infinity Globus

Infinity Globus

21 Jan 2022

21 Jan 2022

1. Introduction

In order to properly optimize your accounting firm’s overall efficiency, effectiveness, and productivity in connection to researching and resolving a tax issue and determining the sustainability of the tax return filing position per Circular 230, the appropriate tax research processes must be meticulously designed, implemented, and executed. The subsequent five comprehensive steps will guide you in establishing an all-inclusive tax research effort on behalf of your entire client base while properly ascertaining the likelihood of success should a tax position(s) taken on a tax return be challenged by the Internal Revenue Service (hereinafter the “Service”) upon examination.

2. Tax Research Methodology

Establish The Facts and Circumstances

The first step in the tax research process is to establish all the facts and circumstances provided by your client in order to determine which tax laws apply to your client’s fact pattern. At this initial stage, it is imperative not to omit nor overlook any of your client’s facts and circumstances whether appearing material or immaterial. Always be guided by the axiom that facts and circumstances appearing to be immaterial individually may, in fact, be material in the aggregate.

Determine All the Issues

The second step in the tax research process entails determining all the tax issues affecting your client’s specific facts and circumstances and any and all mitigating factors. Normally, complex tax issues evolve through several stages of development. For instance, an experienced tax professional based upon his or her prior knowledge of the tax laws, can normally determine most of the initial pertinent issues in terms of general tax laws. However, after performing an initial search of the authorities to answer the initial issues, a tax professional often discovers that one or more additional specific technical questions of interpretations must be resolved before the initial issues can be fully addressed. Consequently, at this stage, a tax professional may also encounter the need to obtain additional facts from the client. Accordingly, the tax research process may have to move back from step two to step one. In addition, you the tax professional may learn at this stage that facts initially not considered to be important may in fact prove critical to the resolution of all your client’s tax issues.

Identify Statutory, Administrative, And Judicial Authority

The third step in the tax research process entails identifying the specific authorities to support all of your client’s tax issues while appropriately weighing authorities that may be contrary to your supporting position. Generally, this process begins with consulting statutory authority (e.g., the Internal Revenue Code) and quickly expands to encompass administrative authority (e.g., Proposed Treasury Regulations, Temporary Treasury Regulations, Final Treasury Regulations, Revenue Rulings, Revenue Procedures, Private Letter Rulings, Technical Advice Memorandum, General Counsel Memorandum, Chief Counsel Advice Memorandum, Circular 230, Internal Revenue Manual, Internal Revenue Bulletins, IRS Field Service Advice Memorandum, IRS Determination Letters, and IRS Notices, etc.) and judicial authority (e.g., judicial interpretations decided by the U.S. Tax Court, the U.S. District Court, the U.S. Court of Federal Claims, the U.S. Circuit Court of Appeals, the U.S. Court of Appeals for the Federal Circuit, and the U.S. Supreme Court). In addition, at times, you the tax professional may have to consult the legislative history (e.g., the Public Laws and Congressional Committee Reports from the House of Representatives and the Senate) of a particular Internal Revenue Code section to fully address what Congress’s intent was in passing a particular bill. Lastly, you may also want to consult the voluminous range of editorial interpretations (e.g., published white papers, published articles, etc.) available to assist in the interpretation a particular tax issue. However, it must be duly noted that editorial interpretations are impermissible sources of authority before the Service and the judicial system. For clarification purposes, the subsequent synopsis will elaborate upon the aforementioned statutory, administrative, and judicial interpretations:

3. Statutory Authority

All federal level tax statutes passed by Congress into law are compiled and published in Title 26 of The United States Code. As it should be recalled, Title 26 of The United States Code contains the specific statutes that authorize the Service to collect taxes for the federal government. Generally, the tax research process begins with consulting the Internal Revenue Code and quickly expands to encompass administrative and judicial authorities based upon the complexity of the tax issue under analysis.

4. Administrative Authority

5. Judicial Authority

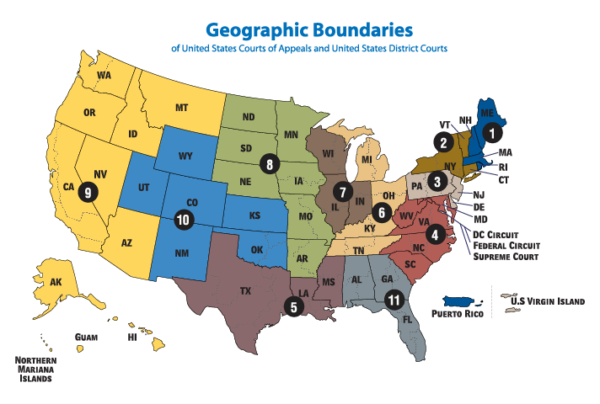

The subsequent chart illustrates the geographic boundaries of The United States Courts of Appeals and the United States District Courts:

6. Resolve the Issues

7. Communicate With Your Client

The fifth and final step in the tax research process entails communicating the conclusion to your client. Your client, of course, must ultimately make the final decision concerning what course of action to take, even though the client’s decision is guided by and often dependent upon the conclusions reached by you, the tax professional. It is strongly recommended that this tax advice be rendered to your client in a written format, as opposed to verbal communication, and preferably in a formal tax advice memorandum format (e.g., Facts & Circumstances Section; Issue(s) Section; Analysis Section; and Conclusion Section) meticulously discussing the applicable statutory, administrative, and judicial authority to suitably document your due diligence in assessing the tax issues(s) and resolving them satisfactorily to reach a strong tax return filing position (e.g., “More-Likely-Than-Not”, “Should”, “or “Will” filing positions). Finally, caveat language in the form of a disclaimer should be documented within the tax advice memorandum for any areas of the tax law that were not within the scope and application of your tax research analysis (e.g., the scope and application of our tax advice memorandum is in connection to the U.S. Federal-Level tax consequences only and does not provide any advice or analysis in connection to any U.S. Multi-State tax consequences nor any advice in connection to Financial Statement Reporting Standards under United States GAAP nor International Financial Reporting Standards).

8. Conclusion

By following the preceding all-inclusive practical steps in the tax research process you should be able to render your tax research services to your entire client base in a more efficient, effective, and productive manner while adequately weighing risk management concerns in connection to the sustainability of tax return filing positions. As a final reminder, the guidance contained in this article should be applied with due professional care including seeking further professional advice from a subject matter expert should it be deemed warranted based upon both the complexity and contentious nature (e.g., taking a tax position contrary to a Treasury Regulation on Form 8275-R, etc.) of the tax matter under review.

Recent Posts

-

The Ultimate CPA Toolkit: 8 Essential Apps to Boost Productivity

infinityglobus | 22 Jul, 2024

-

Exploring the Role of AI in Accounting: Advantages and Downsides

infinityglobus | 15 Jul, 2024

-

CPA Firms Hiring Challenges and How to Overcome Them

infinityglobus | 26 Jun, 2024

-

Accounts Receivable Outsourcing: Why It’s Beneficial for Your CPA Firm

infinityglobus | 4 Jun, 2024